If you’ve received a CP2100 notice from the IRS about a TIN mismatch, it can feel alarming. The language is technical, the deadlines feel urgent, and it’s not always obvious what you’re supposed to do next.

This is not an audit. It’s an administrative flag and it has a clear path to resolution.

TIN stands for Taxpayer Identification Number, which is either a Social Security Number for individuals or an Employer Identification Number for businesses.

When you pay contractors and report those payments on a 1099 form, the IRS checks the name and TIN you submitted against their records. If something doesn’t match — even a small abbreviation or a single transposed digit — the IRS sends a CP2100 or CP2100A notice.

It’s not a bill. It’s not a penalty. It’s the IRS saying the information you reported for a payee doesn’t match what they have on file, and that you need to act on it.

TIN mismatches are more common than most business owners realize. Common causes include a contractor using a nickname instead of their legal name, a recently changed business name that hasn’t been updated with the IRS, a typo on a W-9, or a sole proprietor whose personal name and business name don’t align consistently across forms.

Most mismatches are simple administrative errors, not intentional. But the IRS requires you to respond regardless.

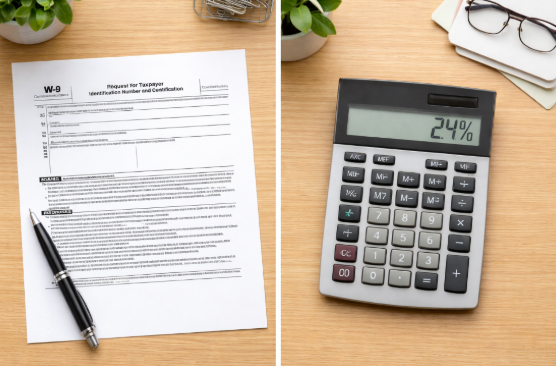

This is the part that gets most business owners’ attention.

When you receive a TIN notice, you’re required to send the affected payee a written notice called a First B Notice within 15 business days. This tells them about the mismatch and asks them to provide corrected information using a new W-9. They have 30 business days to respond.

If they don’t respond, you must begin withholding 24% from all future payments to that person or business and sending that amount directly to the IRS. That’s backup withholding, and it stays in place until the issue is resolved.

Withheld amounts are deposited on the same schedule as payroll taxes and reported at year end on Form 945.

The fastest resolution is usually the simplest one. Ask the contractor to resubmit a corrected W-9 with their legal name exactly as it appears on file with the IRS. For businesses, that’s the name on their EIN application. For individuals, it’s the name on their Social Security card.

If the error was on your end, a corrected 1099 filed with the IRS closes the issue. A CPA or small business bookkeeping provider can handle that quickly.

Collect a completed W-9 before you pay any new contractor — no exceptions. The IRS also offers a free TIN Matching Program through their e-Services portal that lets you verify a payee’s name and TIN before you file 1099s each January. Running your contractor list through that tool once a year can prevent most notices before they happen.

A TIN matching notice is manageable when you act within the 15-business-day window. In most cases, a corrected W-9 or 1099 is all it takes. The businesses that handle these smoothly are usually the ones with a solid process for collecting contractor information upfront.

If you’ve missed the response window, received notices for multiple payees, or aren’t sure whether your backup withholding deposits have been handled correctly, that’s a good moment to bring in a CPA or small business accounting professional to clean it up.